Signup

Plans Starting At $97 Per Month

A credit score is a number generated by a mathematical formula that is meant to predict credit worthiness. Credit scores range from 300-850. The higher your score is, the more likely you are to get a loan. The lower your score is, the less likely you are to get a loan. If you have a low credit score and you do manage to get approved for credit then your interest rate will be much higher than someone who had a good credit score and borrowed money. Therefore, having a high credit score can save many thousands of dollars over the life of your mortgage, auto loan, or credit card.

It's a balance formula. Lets take a look

We will show you how to maximize your debt ratio score, even if paying off credit cards is not an option.

We can also help you to removing credit inquiries from your credit report. Most people are aware of the three credit reporting bureaus, Equifax, Experian and TransUnion. The average difference in scores between the highest and lowest of your credit scores, from the three bureaus, is 60 points. This is the result of the credit bureaus having different items on their report, which may be correct, incorrect or are not reported in full compliance with credit law. According to a recent study, nearly 80% of all credit reports have serious errors on them and this does not even include the even smaller errors for which we look.

If you cannot remove at least 25% of the negative credit items from all three of your credit reports, we will refund 100% of your fee.

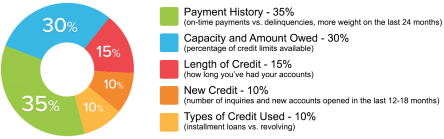

Pay all of your bills on time, every time. This includes your utility bills, mortgage and auto payments, and all of your revolving lines of credit like credit cards. Check your credit report at least once a year. You can find out how to challenge bad information on your credit report here.

Never charge more than 30% of the available balance on any of your credit cards. Banks like to see a nice record of on-time payments, and several credit cards that are not maxed-out. If you are carrying high balances on your credit cards, then make paying them down below 30% a priority. Do use your credit cards – Many people who make mistakes with their credit believe that the best way to fix things is to never use credit again. If you are afraid that you cannot handle your credit cards correctly then the best policy is probably this one: Run only your utility bills on your credit cards each month, and then pay the balance in full by the due date. This ensures that your utility bills get paid on time automatically, and as long as you keep the habit of paying off your credit card balance each month your score will continue to go up. Leave the credit cards locked in a safe or drawer at home.

Keep your accounts open as long as possible – Even if you are no longer charging on the card. The best policy is to keep those unused accounts open, blow the dust off your card every few months to make a small purchase, then pay it off. How long each of your accounts have been active is a major factor in your credit score.

Remember that this all takes time – Following the above steps consistently over a long period of time will increase your credit score and allow you to qualify for better loans and lower interest rates. Repairing your credit score does not happen overnight, so if you do these things for a few months and do not see a large increase in your score, do not give up. They are all habits that you will want to maintain throughout your life, as they will help you to keep your finances and lines of credit under control.

Delinquencies (30- 180 days): A delinquency may remain on file for seven years; from the date of the initial missed payment.

Collection Accounts: May remain seven years from the date of the initial missed payment that led to the collection (the original delinquency date). When a collection account is paid in full, it will be marked as a "paid collection" on the credit report.

Charge-off Accounts: When a delinquent account is sent to a collections company. This will remain for seven years from the date of the initial missed payment that led to the charge-off (the original delinquency date), even if payments are later made on the charge-off account.

Closed Accounts: Closed accounts are no longer available for further use and may or may not have a zero balance. Closed accounts with delinquencies remain for seven years from the date they are reported closed, whether closed by the creditor or by the consumer. However, the delinquency notation will be removed seven years after the delinquency occurred when pertaining to late payments. Positive closed accounts continue to be reported for ten years from the closing date.

Lost Credit Card: If there are no delinquencies, credit cards reported as lost will continue to be listed for two years from the date the creditor is contacted. Delinquent payments that occurred before the card was lost are reported for seven years.

Bankruptcy: Chapters 7, 11, and 12 will remain on one's credit report for ten years from the filing date. A Chapter 13 bankruptcy is reported for seven years from the filing date. Accounts included in a bankruptcy will remain for seven years from the date reported as included in the bankruptcy

Judgments: Remain seven years from the date filed.

City, County, State, and Federal Tax Liens: Unpaid tax liens remain for fifteen years from the filing date. A paid tax lien will remain on one's score for 10 years from the date of payment.

Inquiries: Most inquiries listed on one's credit report will remain for two years. All inquiries must remain for a minimum of one year from the date the inquiry was made. Some inquiries, such as employment or pre-approved offers of credit, will show only on a personal credit report pulled by you.

Information that cannot be in a credit report:

Medical information (unless you provide consent)

Notice of bankruptcy (Chapter 11) more than ten years old

Debts (including delinquent child support payments) more than seven years old

Age, marital status, or race (if requested from a current or prospective employer)

Credit Repair FAQ

Is Credit Repair legal?

Yes, it 100% legal. According to the FTC (Federal Trade Commission) and the FCRA (Fair Credit Reporting Act) a consumer has the right to question and ask for an investigation for every negative item on their credit report.

How long does it take to repair a credit file?

The average credit file takes 3 to 6 months to repair.

How many Credit Bureaus are there and why do I have different credit scores?

There are 3 major Credit Bureaus: Experian, Equifax and Trans Union. All three bureaus act independently and all have their own scoring systems.

What kind of information will I find on my credit report?

Your credit report contains your personal information (name address, date of birth, SS#, etc.); it is made up of your entire credit history, both positive and negative, for the last 7 to 10 years.

What affects my score?

Account Mix: If you have too much of one type of debt this will lower your score.

History: Length of credit history, number of credit card accounts, credit card activity, credit card balances, charge off accounts, late payments, collection accounts, public records, number of inquiries.

What type of balances should I maintain?

Your credit card balance should be between 20-30% of your credit card limit. (eg: If your credit card limit is $1000, your balance should stay between $200-$300)

What are the different types of negative accounts?

Late Payments, Charge off Accounts, Collection Accounts, Public Records (Bankruptcies, Judgments, Tax Liens)

How long does negative information stay on my credit report?

Late Payments: 7 years

Charge off Accounts: 7 years

Collection Accounts: 7 years

Public Records: Judgments: 7 years

Bankruptcies: 10 years

Paid Tax Liens: 10-15 years

Unpaid Tax Liens: Indefinitely

How are negative items removed?

Negative items are removed by requesting the Credit Bureaus to investigate the creditors and verify the negative information they are reporting according to the guideline s in the FCRA.

What if the negative information belongs to me?

The FCRA states that even if negative information belongs to you, if the information contains any inaccuracies, is not being reported and handled according to the guidelines set by the FCRA or cannot be verified in its entirety, then by law it must be removed. Statistics show that inaccuracies occurs more than 70% of the time in a credit file.

Is the removal permanent?

Yes

What happens if negative information is re-inserted?

This rarely happens. There are consumer laws to protect you from negative information being re-inserted to your credit file, but in the event that it does, these same laws are used to have the information removed permanently.

If I pay an outstanding bad debt will it be removed from my credit report?

No. it will now begin to report as a paid debt and will have a reporting life of 7 years.

If I bring my credit card balances to zero will my scores go up?

Temporarily and then they will drop again. Credit scores are partially based on credit activity. If there is no activity it negatively affects your credit score.

How do I start the credit repair process?

Pull a recent copy of your credit report and then have a consultation with one of our credit repair specialists.

What is my obligation as a client?

Pay your bills on time and try not to add any additional negative accounts to your credit file while it is being repaired. You must follow the individual advice of your credit consultant; remember they have your best interest in mind. Furnish the necessary documents requested by the Credit Bureaus and return all responses you receive from the bureaus in a timely fashion or your credit repair process will be delayed. The bureaus will not accept responses for re-investigation that are more than 3 months old.

How long before I see results?

One of the most common and normal questions to ask is "how long is it going to take to see results?" The honest answer is that it all depends on your situation and how much work you need done but most Credit Repair Mangers clients begin to see some results within the first 30-45 days. That's why working with a professional credit repair manager from our network is the best choice for your credit repair needs. We assign a certified financial and credit expert to review your credit report and build you your own personal plan. Your plan focuses on the areas that will make the most impact on your overall credit profile. We will mark the accounts by severity so that you can see yourself which ones are impacting your score the most.

What if all my negative items are accurate?

At Credit Repair Managers we work by removing inaccurate negative items from your credit report. However, some negative remarks are substantiated and many clients wonder what happens in this case. There is still room for improvement! Negative, inaccurate, and erroneous remarks have more to them than meets the eye. Credit card companies will often times share critical information about your financial life. This may include information about your car payments, mortgage, employment and family obligated payments. In these instances our certified Credit Repair Manager goes to work and evaluates the validity of this information. It is our job to assess the information and the items on the credit report. So, see what the process can do for you. It might surprise you how much is possible.

Can you help while I'm going through a bankruptcy?

One of the most important things to consider while filing for bankruptcy is how to properly manage your credit. Bankruptcy is a crucial time for understanding your financial standing. Mistakes during this process can result in negative financial standing for much longer than necessary. When someone files for bankruptcy, it is very easy for information to be mishandled as it passed through the numerous reporting agencies resulting in incorrect and mistaken reports. Your Credit Repair Managers team is a mainstay for individuals filing for bankruptcy as they can help you navigate the system. This financial decision does not have to bring extended repercussions. When you're dealing with something like bankruptcy, it feels good to know that experts who are skillful and trustworthy are looking out for you.

Is credit repair worth it? Why?

Good credit standing can lower everything from car payments, mortgages, and business loans. Employers often run credit checks before making hiring decisions. Not having an ideal credit score will impact all areas of your life and stand in the way of improving the various aspects of your life. Taking control of your credit report and credit score will allow you to take advantage of the positive opportunities in your life. The savings that will result from increasing your credit score will greatly outnumber the initial investment into your credit. Credit Repair Managers works to help you with all types of credit problems by charging only $ a month. This initial investment into your credit history will allow you to continue to reap the benefits long after you finish making payments.

Do you offer debt settlement?

Credit Repair Managers works to repair your credit. This is different from the services that debt settlement companies offer. Settling with credit card companies refers to settling on a mutually agreed debt payment and then taking on the responsibly of paying that amount. At Credit Repair Managers we work to dispute those charges rather than agree to pay erroneous charges. By settling with debt collection agencies, this can have an additional negative impact on your credit score and report. If the goal is to improve your credit, than you need an experienced credit company to ensure that those items on your credit report are accurate and correct before being reported.

What are the costs associated with your service?

There are two fees associated with starting the process. First step is to pull your credit report; this is $1.00 for all 3 Credit bureaus. The costs to providing these services and starting to increase your credit score is only $ per month. There are no additional costs or hidden costs.

Where are your offices located, do you have an office in my area?

We are based in Los Angeles California with offices in several other states around the country as well as international representatives. Our Financial and Credit advisers are available by phone and email and will respond to inquiries within 24 hours, during the week as well as the weekend.

What are the hours I can speak with a Credit Repair Managers Adviser?

Sometimes you just want to talk to somebody - to ask questions, get encouragement or understand the process better. And we're here to talk to you, during the following hours:

Call 1-833-201-1257

M-F 8 AM to Midnight EST

Sat 9 AM to 7 PM EST

Sun 11 AM to 7 PM EST

What is the Fair Credit Reporting Act and why was it created?

The Fair Credit Reporting Act (FCRA) was written as an amendment to the Consumer Credit Protection Act. It provides consumer protection that ensures that the information presented on your credit report is accurate and correct. It allows you to personally contact the credit bureaus or hire a representative to contact them on your behalf. That is where Credit Repair Managers comes in.

What are the three credit bureaus?

A credit bureau - sometimes called a "consumer reporting agency" - is a business that collects relevant consumer information from creditors and courthouses, and then sells that information to interested parties such as potential lenders. Such information is sold in the form of a credit report. In the U.S., the three major credit bureaus are TransUnion, Experian, and Equifax.

How long does it take to fix bad credit?

One of the most common and normal questions to ask: how long is it going to take to see results? The honest answer is that it all depends on your situation and how much work you need done but most Credit Repair Managers clients begin to see some results within the first 30-45 days. That's why working with Credit Repair Managers is the best choice for your credit repair needs. We assign a credit expert to review your credit report and build you your own personal plan. Your plan focuses on the areas that will make the most impact on your overall credit profile. We will mark the accounts by severity so that you can see yourself which ones are impacting your score the most. You can also change the severity of an account and Credit Repair Managers will alter your plan accordingly.

What is a credit repair company and how can they help you?

We at Credit Repair Managers are here to represent and advocate on your behalf. Our expertise and constant communication with the credit bureaus ensures that we obtain the best results possible.

How long do negative items stay on your credit report?

Negative items on your credit report do not have a specific shelf life. It is up to the creditors to decide how long negative remarks stay on your credit report. Credit Repair Managers works to remove these remarks as soon as possible..

Plans Starting At $97 Per Month

See updates, online client portal dashboard

Contact

Call-Text:1 424 999 9756

Toll Free 1 888 347 0609

SUBSCRIBE

Get updates and free resources.

Mobirise web page builder - Find out